In 2023, European startups secured approximately $60 billion in venture capital (VC) funding, showcasing the continent's dynamic innovation landscape. This funding performance, detailed in a report by global law firm Orrick, highlights the shifting tides of investment preferences and strategic adjustments startups are making in response to broader market conditions.

Sector Spotlight

The artificial intelligence (AI) sector commanded a significant portion of the total VC funding, securing a 17% share. This indicates the growing importance of AI technologies across various industries. However, climate technology (climate tech) emerged as the frontrunner, overtaking AI in terms of investment popularity. The focus on climate tech underscores Europe's commitment to sustainability and the growing investor interest in environmentally-focused innovations.

Changing Dynamics in Financing

There was a noticeable downturn in later-stage financing, attributed to founders exploring alternative financing routes or pivoting their business models towards profitability. This shift reflects the strategic adjustments companies are making in a tightening funding environment. Early-stage deal values also experienced a 40% decrease, signaling a cautious approach from investors towards newer ventures.

Investment Terms and Trends

Market conditions have led to venture capital deal terms that largely favor investors, allowing them greater control over investments. A notable 23% of funding rounds involved convertible financing mechanisms, such as convertible debt, Simple Agreements for Future Equity (SAFEs), and Advanced Subscription Agreements (ASAs). Furthermore, in 39% of venture deals, investors required founders to provide warranties, highlighting the increased scrutiny and due diligence being exercised in the current climate.

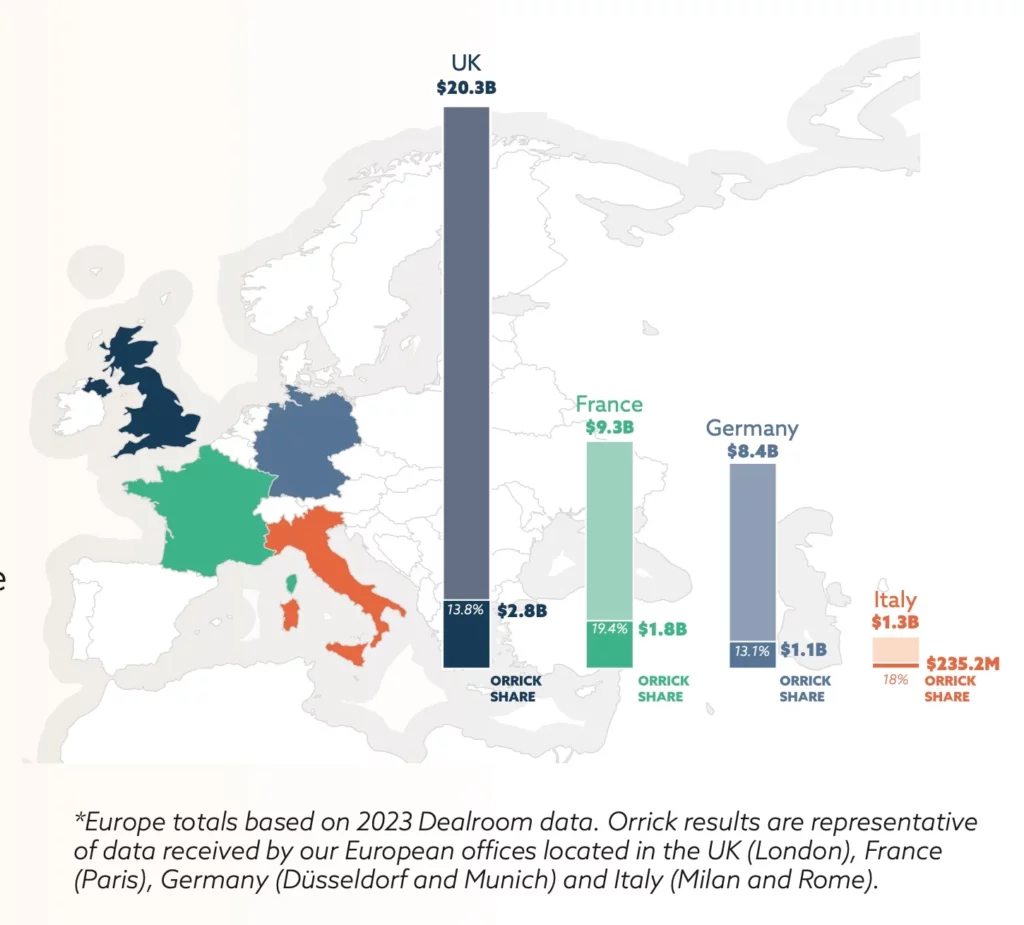

Regional VC Pressures and Opportunities

The report also touches on regional nuances affecting VC activities. In the U.K., venture capitalists are experiencing pressure, prompting a pivot towards secondary markets and an increased focus on mergers and acquisitions (M&A) within their portfolio startups. Similarly, in Germany, there is an expectation of a surge in M&A activities driven by Limited Partners (LPs) demanding liquidity. These trends indicate a strategic shift in investment approaches, with a clear inclination towards consolidating assets and unlocking value through mergers and acquisitions.

Conclusion

The European startup ecosystem, while navigating a complex set of challenges, continues to attract significant investment, particularly in sectors poised to shape the future, such as climate tech and AI. The adjustments in financing strategies and the evolving investment terms underscore a broader market adaptation to ensure resilience and growth. As startups and investors alike recalibrate their strategies, the emphasis on sustainability, innovation, and strategic mergers and acquisitions is likely to define the trajectory of the European startup landscape in the years to come.