The venture capital ecosystem is currently experiencing a significant slowdown, primarily due to a notable scarcity of exits, particularly large-scale tech public listings. In the first quarter, the total U.S. VC exit value stood at a mere $18.4 billion, with the IPOs of Reddit and Astera Labs making up roughly three-fourths of this figure. Although these IPOs generated considerable media buzz, it's still premature to declare them as indicators of a reinvigorated public listing environment.

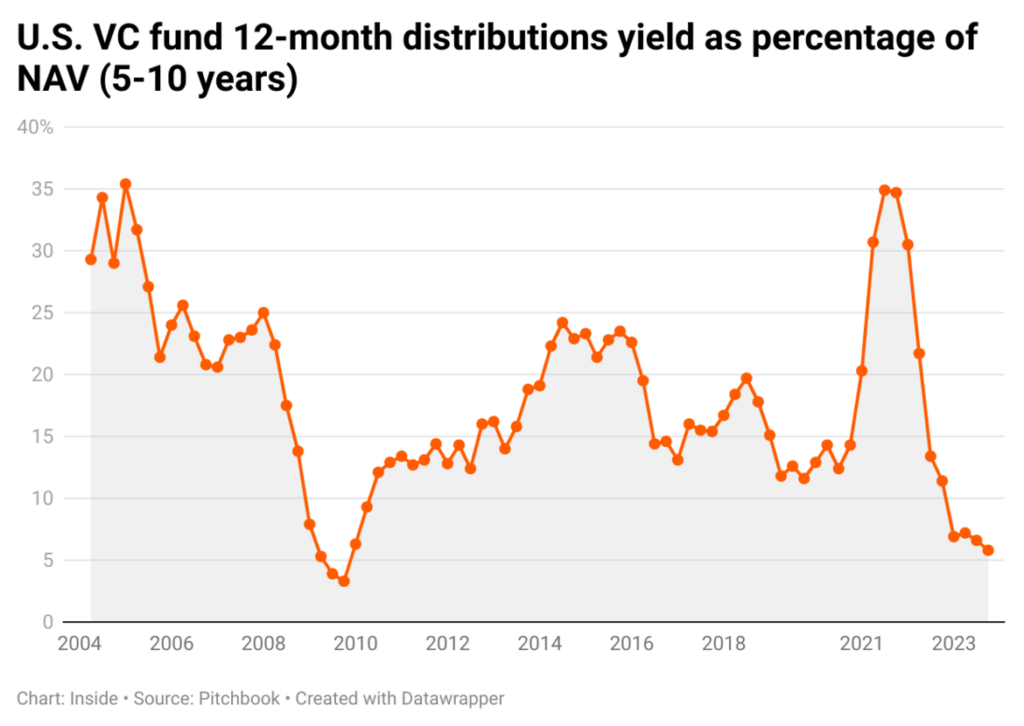

Over the past two years, the exit market has been lackluster, causing many General Partners (GPs) to struggle to turn paper gains into actual cash distributions to Limited Partners (LPs). This situation has been exacerbated by many institutional investors facing liquidity constraints amid an ongoing market correction. With a generally low Distribution to Paid-In (DPI) ratio, LPs have found themselves unable to recycle distributions back into commitments to venture funds. This has led to a continued slowdown in fundraising activities, with only $9.3 billion secured across 100 venture funds.

In response to these market conditions, many venture capitalists have postponed their next fundraising timelines, choosing instead to concentrate on their existing portfolios and being exceedingly selective with new deals.

The market is yet to see a significant recovery, despite some stock market rallies starting from late 2023. These rallies were largely driven by a small group of leading tech companies, optimism surrounding potential interest rate cuts, and excitement around advancements in AI technology. However, with the latest inflation figures coming in hotter than expected, it's unlikely that the Federal Reserve will initiate rate cuts before the second half of 2024. Even then, the extent and speed of these cuts remain uncertain, affecting the valuations of public companies and influencing the exit strategies of late-stage startups and venture-growth firms.

Historically, mergers and acquisitions (M&A) have dominated the exit landscape. Given the pressing need for liquidity across the capital table and a gradual alignment on pricing between founders and investors, we expect to see an increase in acquisition activities. This uptick will likely be fueled by strategic buyers like corporations and private equity firms, along with sector-specific tailwinds that could energize the market.