Great lockdown recession is often compared with 2009 crisis and predicted to be the worst economic downturn since The Great Depression. According to IMF report in June, global growth will fall by 4,9 percent; global economic recovery is expected to be 5,4 percent in 2021, but this forecast might work only if pandemic fades in the second half of 2020. All three IMF scenarios infer negative dynamics for 2020 and uncertain growth in 2021, depending on COVID-19 possible outbreaks.

Venture capital investments is being on a list of sensitive spheres instantly responding on every economic turmoil. However, the research, provided by EXPERTORAMA in partnership with Unicorn Nest, displays that investment funds are more optimistic about the end of crisis, comparing to IMF data.

Losses and reduction

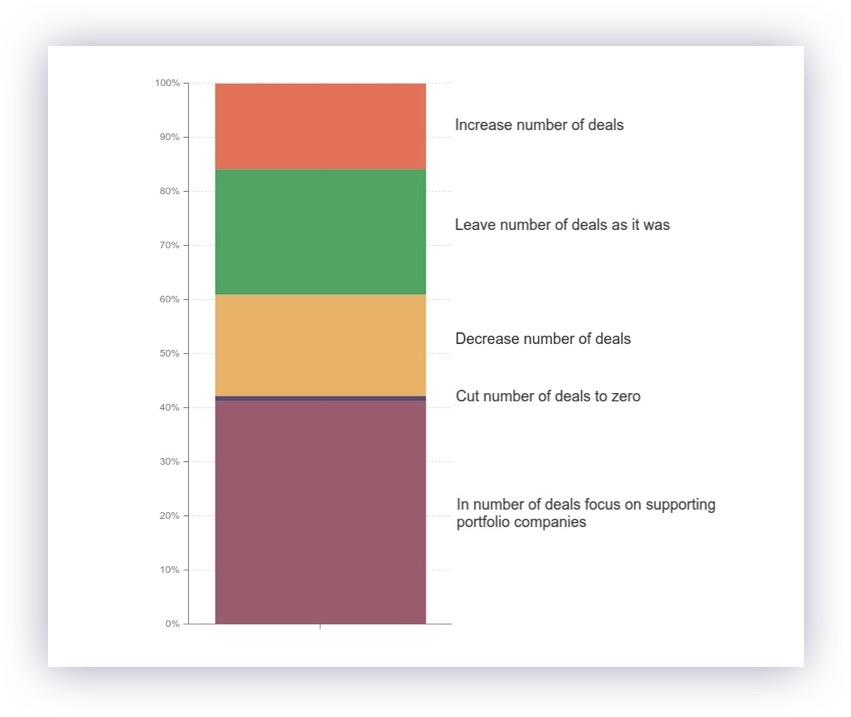

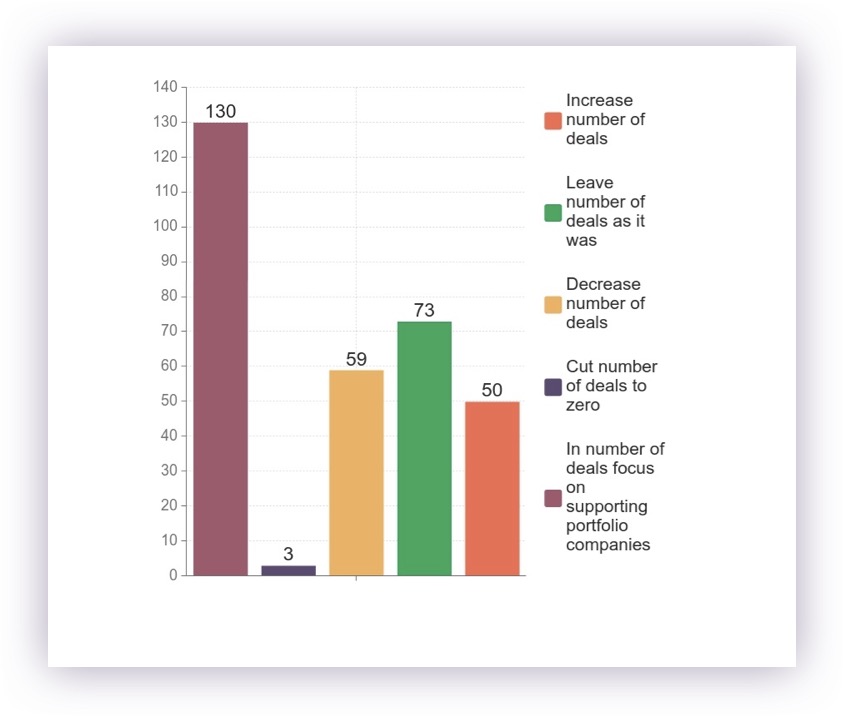

Based on research provided with surveying 250 funds mostly in North America, Europe and Asia, almost 19% of representatives decreased number of deals. On the other side, only 1 percent cut the deals completely and investment pause is focused on pre-seed, seed, H-series and angel funding types. Obviously the most affected industries were travel, HR, parenting, personal health and diagnostics, market research and real-time.

In terms of changes of average check VC funds got 23 percent decreasing rate for industries related to social connections, such as service industry, fitness or B2B. Focusing on specific amounts funds spent less in round size investment for startups in ranges of 1-5M, 5-10M and 50-100M. The smallest and the biggest ranges (up to 100k and 100M above) faced no negative changes in investment size.

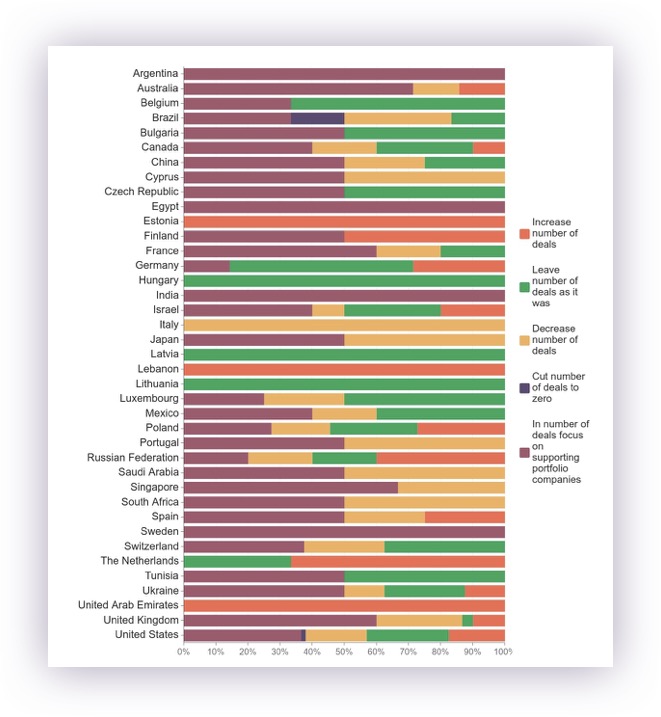

Geographical allocation is correlated with overall level of COVID-19 impact on each country. Top-5 decreases are Italy, Portugal, South Africa, Saudi Arabia and Cyprus. All of them not only reduced number of deals, but shown none of positive dynamics in leaving planned deal or increasing its number.

New crisis, new opportunities

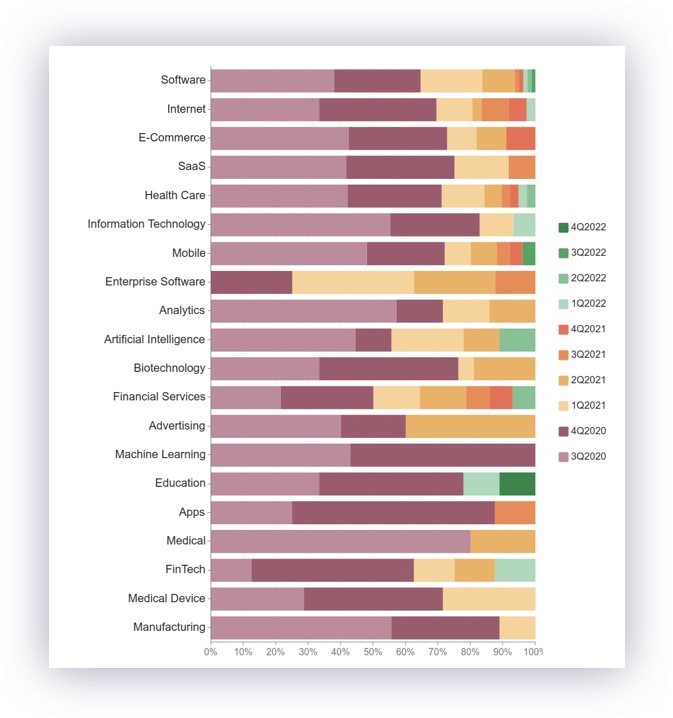

As almost 1/5 of funds were forced to reduce investing level, another 15 percent of respondent increased number of deals with average check growing on 17%. The most attractive industries for crisis investments were education, biotechnology, machine learning, information technology and Saas. Estonia, Finland, The Netherlands and UAE specifically focused on new investments with ranges 100k-1M (35% increasing average check) and above 100M of investments (65% increasing average check).

How far would crisis go?

VC funds predict the end of crisis peak this year. Among all interviewed funds more than 65 percent believes that peak will be passed by 3Q and 4Q 2020. A quarter of respondents are less optimistic and bet on first half of 2021. Among all audiences no one believes that crisis peak could possibly be passed in 2023-2025.

Developing countries are expectedly more careful in forecasting, while none of funds based in UAE, Cyprus, China, Spain, Singapore and Saudi Arabia responded far then 4Q of 2020.

Industries such as IT, machine learning, apps, education manufacturing and medical device are on a list of top-attracted this year, but 2021-2022 might offset them in face of more interesting adds, enterprise software, financial services and fintech.

In order to provide unbiased analysis, EXPERTORAMA contacted survivors of 2008-2013 financial crisis with the same questions regarding end of the peak. Interviewed funds basically showed the same responds as non-experienced investors: 60 percent believes that peak will be passed by the end of 2020, a quarter is looking more to first half of 2021. List of interests differs a little, as this year survivors concentrate on medical, pharmaceutical, medical device, ads and education. In terms of cutting deals or reducing/increasing check amounts 2008-2013 crisis veterans got almost the same statistics, as newbies. As a conclusion in can be seen, that all VC-funds despite their years on market provide the same results on investment field. The only point that differs significantly is spheres of interest for 2020, though in 2021 they consolidate again.

Conclusion

As Unicorn Nest is the biggest open VC-funds base in the world, our specialists were able to provide analysis on 39 000 funds, identifying 28 major clusters. All of them differs according to more than 100 indicators and are operated by a list of unobvious principles. As an example, two of clusters can be dissected:

#11 cluster got the following features:

- Funds founded in 2014 – 2016;

- Located mostly in Asia;

- All of them are Institutional VC;

- Mostly invest in a country of their foundation;

- Mostly invest in Early Stage and NonEquity Assistance and Initial Coin Offering and never take part in Grant stage.

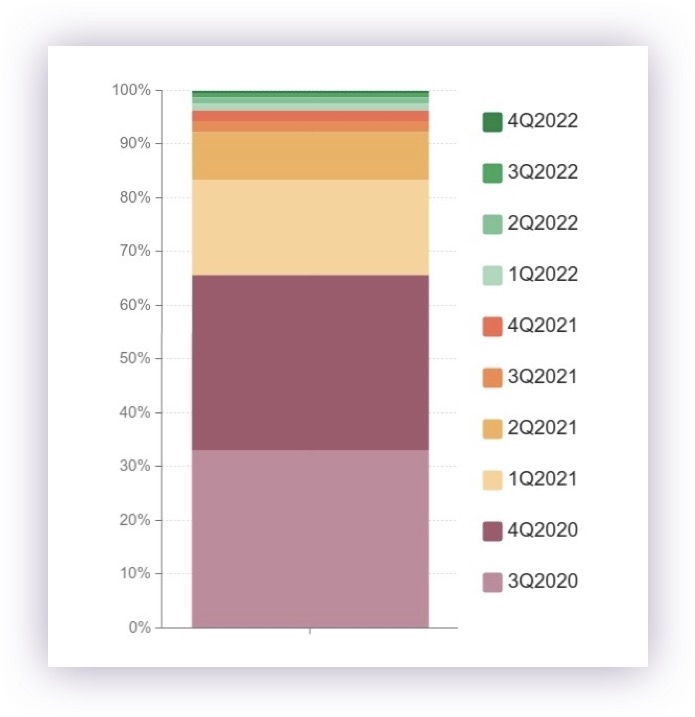

Funds of this cluster have a quite short history of successful exits: most of the exits were performed in 2014, 2018 and 2019 - 2018 became a year with maximum deals for them. According to the provided research #11 cluster funds believes that crisis peak would be passed in 3Q2020. Less of them bet on 4Q2020, but none of representatives expect the peak to be in 2021 or later. However, this cluster got a tendency in decreasing average check and no positive dynamics in new number of deals.

Opposite to that #4 cluster consists of experienced VC-investment veterans with the following features:

- Founded in 1998 – 2001;

- Located mostly in North America;

- About 80 % of them are Institutional VC;

- Mostly invest in a country of their foundation;

- Mostly invest in Non-Equity Assistance, Early Stage, Late Stage;

- Also, they would prefer Late-stage investment in rounds among Seed and Early stages.

Despite #11, this cluster got 2000 as a year with maximum deals, with an increasing of deals in 2004 - 2008, but with no high activity in recent years. #4 predict the end of crisis peak in 1Q2021 or even 3Q2021. Only a small amount of funds believes in 3Q2020, but none of funds in this cluster cut the deals or average check sum.

Being full of variety, venture ecosystem could be influenced by a trend deeply hided from non-professional experts. Thus, it might be hard for a freshman to understand all casual relations in specific field. Based on two completely different clusters - #11 and #4 these undercurrents can be displayed.

For additional information public version of a mentioned report can be checked via this link.