Startups often underestimate their chances to find cross-border investments and receive funding for the required purposes. UN decided to learn more about the reasons and consequences of such decisions and interviewed 230 funds around the globe to find out how cross-border deals work for them, what spheres of interest attract VC-funds, where they prefer to invest, on what stages, and much more information. This research aimed to be useful both for startups and for investors to see key directions for cross-border deals and might help to review the investment strategy.

Cross-border is a new black

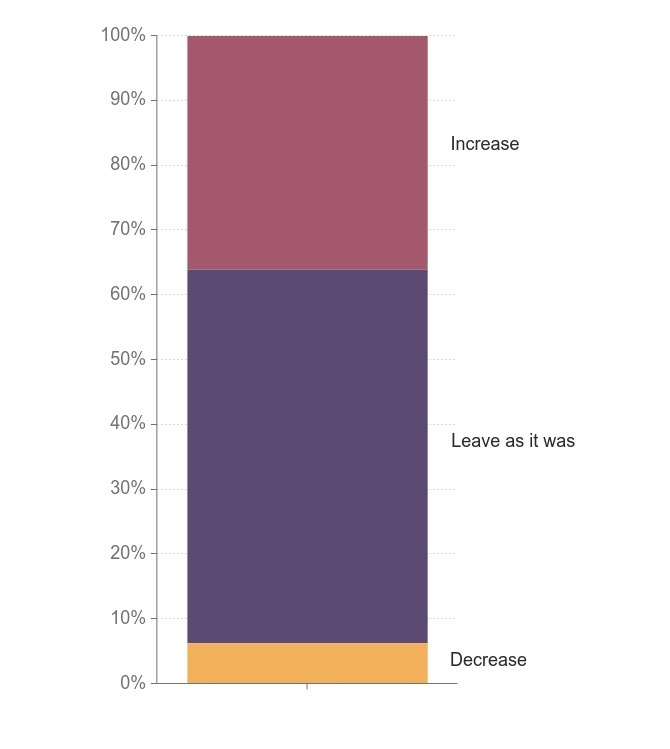

According to the research, only 6% of funds are going to reduce the number of cross-border transactions, while 36% are going to increase it. This means COVID-19 crisis might have a short-term impact on investment plans now, but ⅓ of funds will increase their investments in the nearest future.

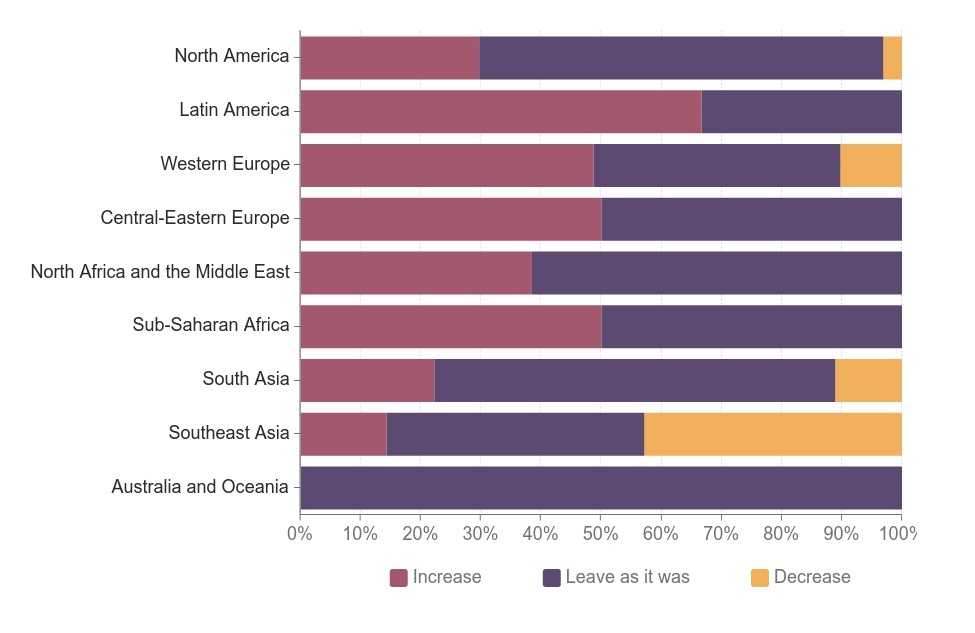

Funds from Latin America, Western Europe and Russian-Eurasian regions are top-3 countries of funds origin which plan to increase the number of cross-border deals. The most interesting regions for investors are Latin America, Central-Eastern Europe and the MENA region. The least interesting (planned to reduce) are Southeast and South Asia, along with Western Europe.

Seed stage attracts 50% of investors, while only 15% are interested in the late stage. However, cross-border investments are not as often, as domestic are: mostly VC-funds make up to 4 investments per year (60%) and less than 10% of respondents can provide above 20 deals annually.

The most popular spheres VC-funds plan to increase investments are software, e-commerce, IT, financial services, education analytics and biotechnology. The “outsiders” which are going to be reduced are travel, fashion, HR, video, digital entertainment, energy and peer to peer.

Talking about amounts of investments and VC-funds plans for it, the average investment round size would be 100% increased in 50-100 mln. diapason and 10% reduced in 100k-1mln and 5-10 mln. As can be seen from these data, cross-border deals got a huge potential to grow and definitely will increase this and the following years. But how do investors decide where to invest particularly? UN got the answers.

Decision points of cross-border deals

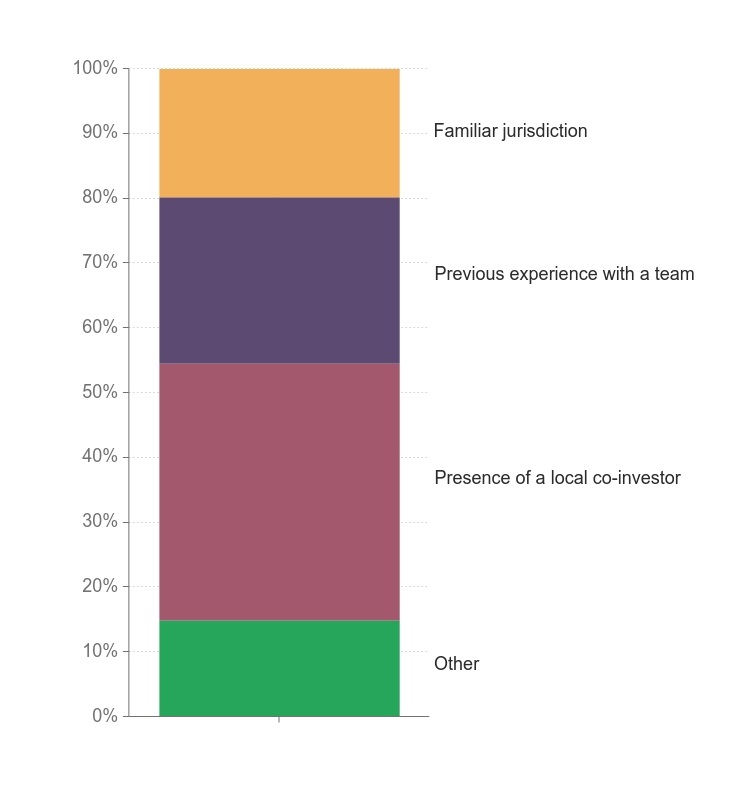

Working with a foreign startup requires additional research for VC-fund as there might be a significant difference in the legislative base, taxes, accounting, state policy an inner country climate. UN classified three main points for decision-making:

- Familiar jurisdiction;

- Previous experience with the team;

- Presence of local co-investors.

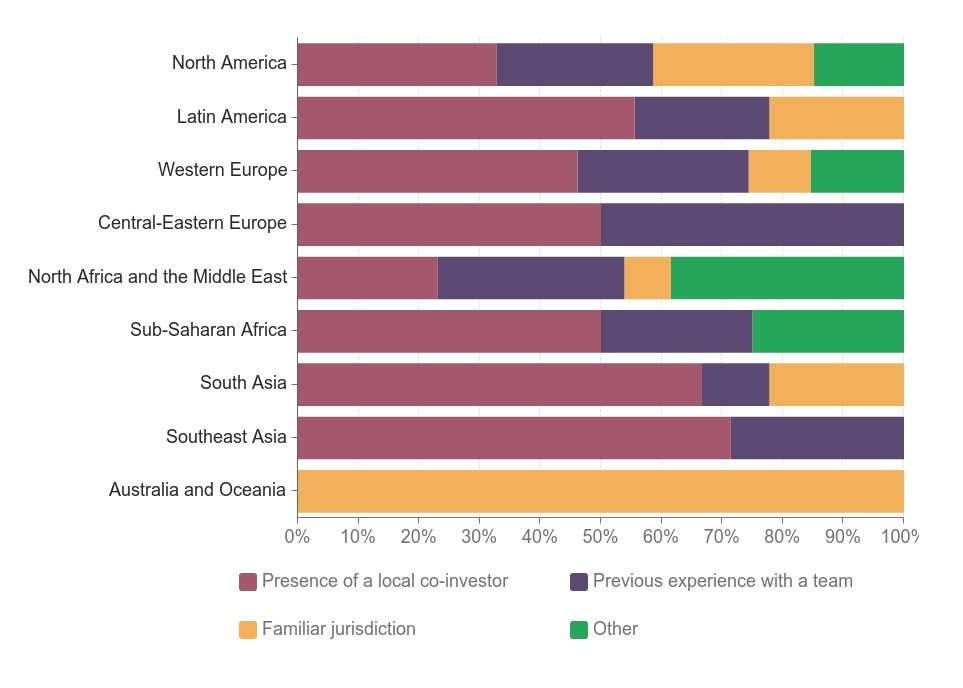

Together these three points cover 85% of the factors that influence the opinion to invest or not. 15% left are shown as category “others” as this amount consists of various factors too small to be considered as a separate value. Among this 85% the most important is local co-investor (40%), then the past experience of work (25%) and 20% goes to familiar jurisdiction.

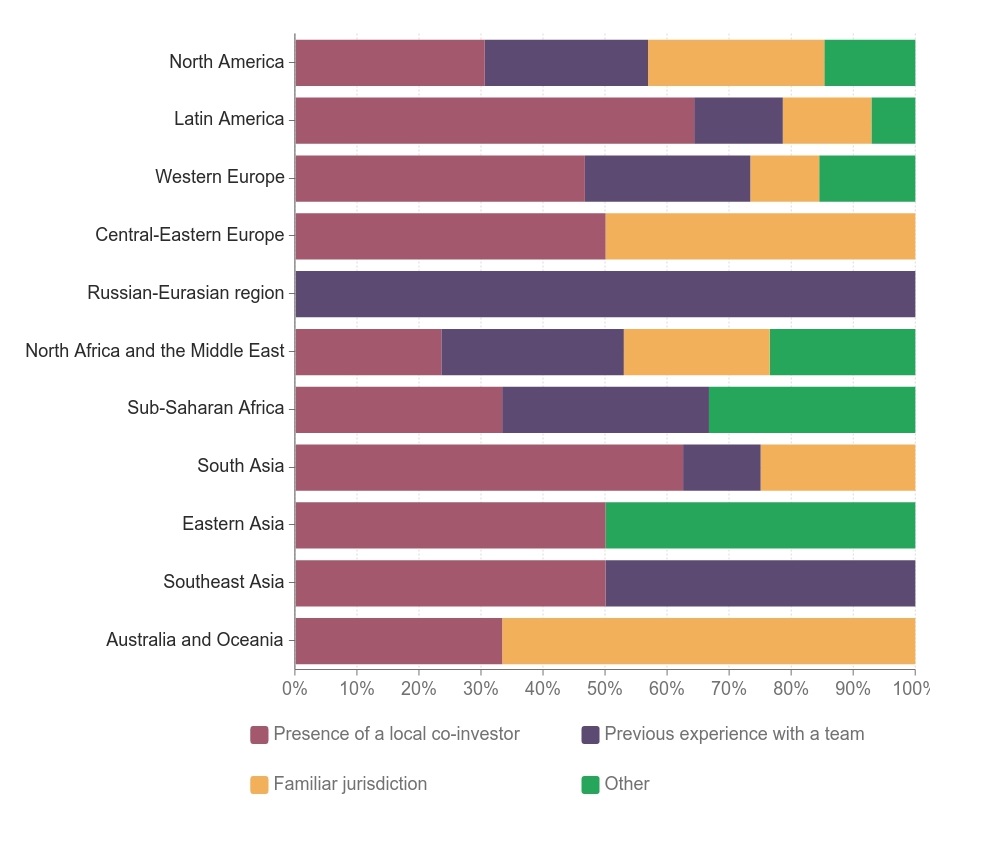

Geographical spread differs a lot from region to region. For example, Russian-Eurasian region funds (participated in the interview) invest only in teams they have worked together with already. Southeast Asia funds divided 50% to 50% with presence of co-investors and previous experience. Familiar jurisdiction is extremely important for funds from Central-eastern Europe and Australia/Oceania (over 50%).

In terms of countries where to invest this stratification becomes even more interesting: jurisdiction is 100% most important if VC fund goes to Australia/Oceania market, South and Southeast Asia got 70% for local co-investors and Central-Eastern Europe startups got a higher chance to succeed if they already worked with a fund (50% of funds answered that past experience is crucially important for them if they invest in Asian companies).

A sphere of investment also depends on three points mentioned above. For example, health care, digital media, cryptocurrency, EdTech and market researchers are close to familiar jurisdiction. At the same time, VC-funds with previous experience with the team prefer to invest in semiconductor, computer, security, marketing, retail and entertainment.

For unicorns, it is important to find local co-investor, as this point is confirmed both by investors and by 2019 proclaimed unicorns experience.

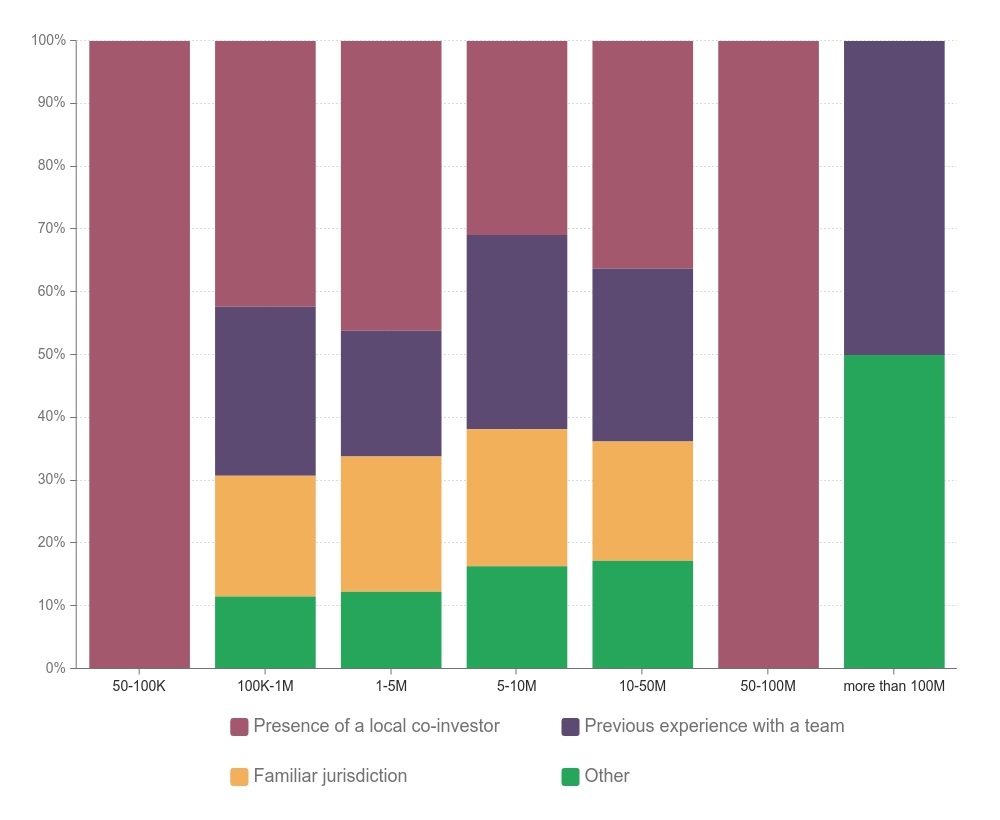

The average investment round size is got the following trend:

- Local co-investor is 100% important for sums 50-100k and 50-100m;

- Investments more than 100m are influenced by previous experience (50%) and 50% marked as “other”;

- From 100k to 50m familiar jurisdiction got an average number of 20-25% according to the interviewed investors.

Thus a basic recommendation for a startup looking for cross-border investment is to find a local co-investor or a fund familiar with the state legislative base.

How they invest: who and where to?

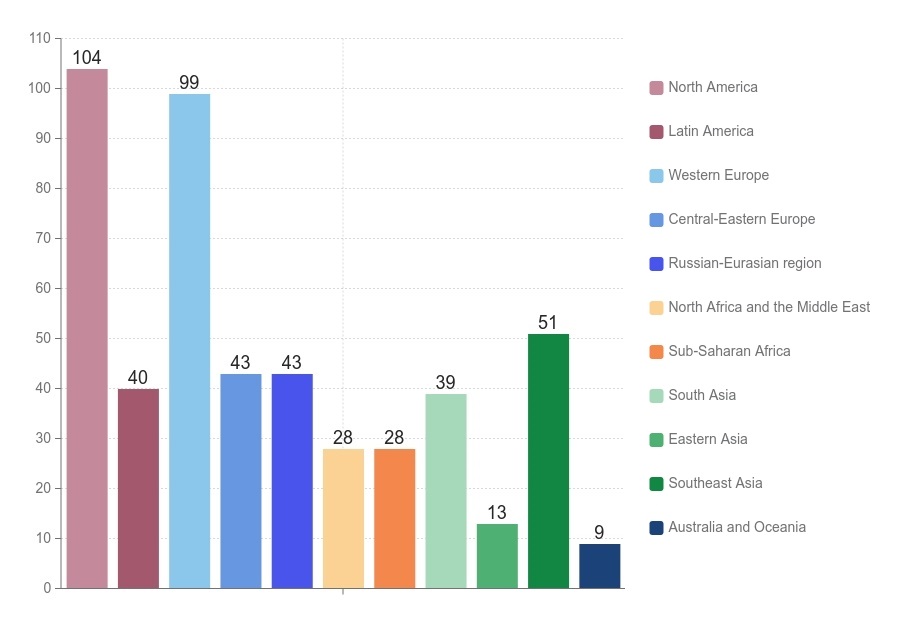

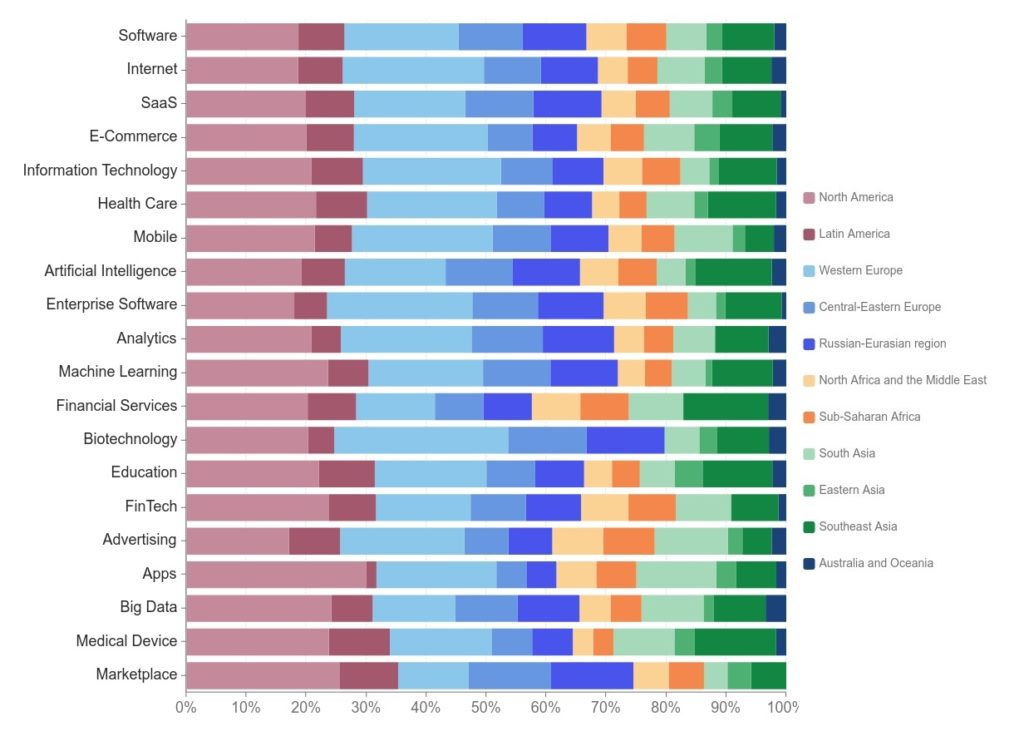

According to VC-funds answers, future cross-border deals would be done in North America (21%), Western Europe (20%), Southeast Asia (10%), Central-Eastern Europe (8%), Russian-Eurasian region (8%), Latin America (8%), South Asia (8%), North Africa and middle east (6%), Sub-Saharian Africa (6%), Eastern Asia (3%) and Australia/Oceania (2%).

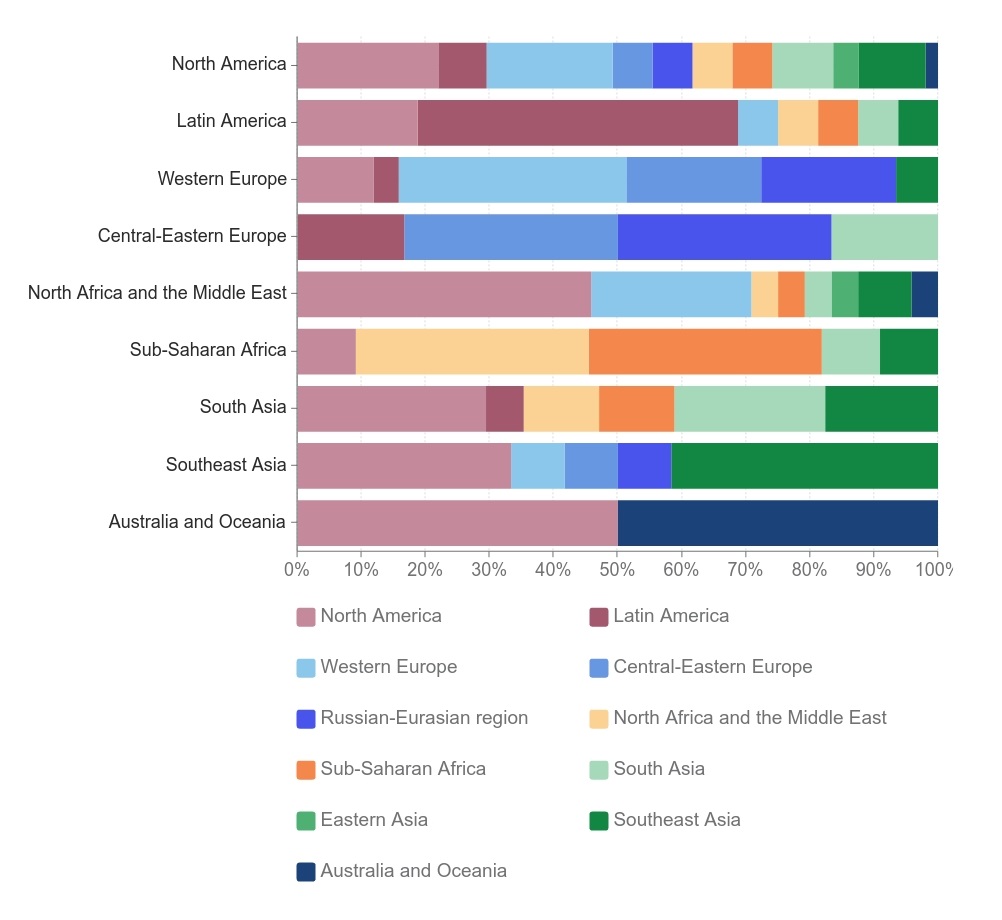

A huge investment inside the domestic region remains:

- Startups from Australia/Oceania are invested by North American and local VC-funds (50% to 50%);

- Southeast Asia got up to 40% of investments from the countries situated in the same region;

- Europian startups receive more than 45% from Western or Central-Eastern Europe;

- At the same time Central-Eastern Europe companies are close to Russian-Eurasian investors and got almost 35% of funds from that region;

- 65% of investments for Sub-Saharah Africa come from this region or Middle East.

Allocation in spheres of interest is common for every region with two anomalies: European and Russian-Eurasian venture funds are more interested in biotechnology than other regions and Asian and Middle East funds are looking for the financial services industry.

Western Europe funds are top investors in 2019: among regions that provided more than twenty-one deals, they got almost 30%. The second place goes North America with 20% and South Asia with a little less than 20%.

Recommendations and conclusions

If a startup is going to find cross-border investment, there is a simple check-list:

- Pay attention to the number of fund’s portfolio startups’ exits with valuation $100-500M - this fund might increase the number of cross-border deals;

- Local co-investor decreases the significance of a familiar jurisdiction and other points, so it might make it easier to receive funding by involving local VC find along with foreign investor;

- Previous experience with a team is a “power move”, but lack of such an experience excludes deals only when it goes to over 100m in the round size;

- Up to ⅓ of cross-border deals are done withing one region, so regional funds should be checked firstly;

- Pay attention to the spheres of interest and the number of cross-border deals in a particular region.

The statistics unhesitatingly say that number of cross-border transactions will increase in every region, the spheres of investors’ interest are various and even jurisdiction cases can be solved. Therefore, the eternal question “to do or not to do” transforms into practical “when and how”.

Cut-version of the research can be also found via this link.